- The Business Bulletin Newsletter

- Posts

- Assets that are keeping you poorer in 2025.

Assets that are keeping you poorer in 2025.

Why Your House, Car, and Savings Are Destroying Your Financial Future”

Hey there, future wealth builders!

I’m about to crush some dreams today, and I’m not sorry about it.

You know what’s wild? We’ve been brainwashed into thinking certain things are “assets” when they’re actually wealth destroyers in disguise. These financial vampires are sucking your money dry while you smile and pat yourself on the back for being “responsible.”

Today, I’m pulling back the curtain on the biggest money lies of 2025. These aren’t just bad investments - they’re wealth killers that are keeping you trapped in the middle class while you think you’re building wealth.

Ready to have your mind blown? Let’s dive in.

The American Dream That’s Actually a Nightmare: Your House

Oh boy, here we go. I can already hear you typing angry comments, but hear me out.

Everyone’s been told that buying a house is the ultimate wealth-building move. “Build equity! Stop throwing money away on rent!” Sound familiar? Well, I hate to break it to you, but for most people, their house is the biggest money pit they’ll ever own.

Let’s do some real math here. You buy a $400,000 house (which is pretty average these days). You put down $80,000 and feel proud of yourself. But here’s what nobody tells you:

You’re about to spend 3-4% of your home’s value every year just keeping it from falling apart. That’s $12,000 to $16,000 annually - and that’s BEFORE your mortgage payment. New roof? $15,000. HVAC system dies? $8,000. Plumbing disaster? $3,000. It never ends.

But here’s the kicker - that $80,000 you put down? If you had invested it in boring old index funds earning 8% annually, it would be worth about $173,000 after 10 years. Meanwhile, your house might appreciate 3% per year, but after all the costs, repairs, taxes, and insurance, your real return is basically zero.

And don’t even get me started on the opportunity cost trap. Your wealth is literally trapped in your walls. Need money? Too bad - you can’t sell just the kitchen. You either take out another loan (more monthly payments) or sell the whole house, which takes months and costs 6-8% in fees.

The worst part? Most people put 80% of their net worth into one asset in one location. If your local market crashes or you lose your job, you’re toast.

I’m not saying never buy a house. I’m saying stop pretending it’s an investment. It’s a lifestyle choice that usually costs you wealth, not builds it.

The Money Shredder in Your Driveway: Your Car

Let’s talk about the most expensive thing you’ll never admit is destroying your wealth: your car.

Americans have convinced themselves that cars are assets because they have “value” and you can sell them. That’s like saying a melting ice cube is an asset because it’s still technically ice.

Here’s the brutal truth: A new car loses 20% of its value the moment you drive it off the lot. After one year, it’s worth 70-80% of what you paid. After five years, it’s worth less than half. You’re literally watching your money evaporate in real-time.

But wait, it gets worse. The average American spends $9,000 per year on car-related expenses. That’s $90,000 over 10 years for something that’ll be worth maybe $5,000 at the end. It’s like setting $85,000 on fire, but slower.

And most people finance these depreciating disasters! They take out 6-7 year loans to afford newer, more expensive vehicles. You’re literally making payments on something that’s losing value every single month. For years, you owe more than the car is worth.

Here’s what smart people do: They buy reliable used cars with cash and drive them until they die. That $500 monthly car payment invested at 7% over 30 years becomes about $500,000. Your fancy car becomes worth nothing.

Which would you rather have: a shiny car that impresses strangers at red lights, or half a million dollars?

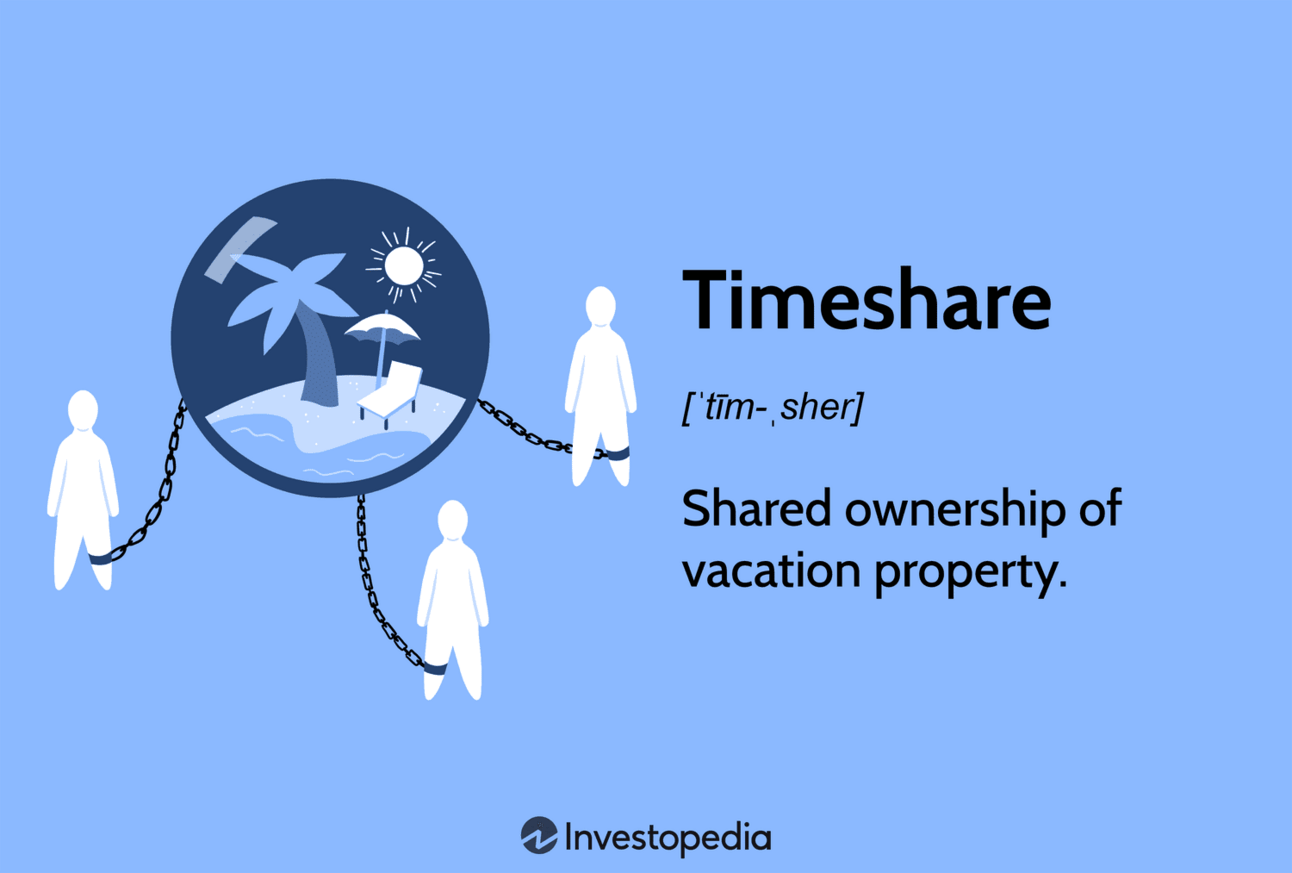

The Vacation Scam That Never Ends: Timeshares

Oh, timeshares. The financial equivalent of a zombie - they look alive, but they’re actually dead and will eventually eat your brains.

These are sold as “real estate investments” that pay for themselves through vacation savings. In reality, they’re one of the worst purchases you can make. Most timeshares lose 80-90% of their value immediately and come with fees that increase faster than your will to live.

When you buy a $30,000 timeshare, you’re not buying real estate. You’re buying the right to use a property for one week per year at resort prices. You could stay at that same resort as a regular guest for way less money.

But the maintenance fees are where they really get you. These start around $800 per year and increase every year, often faster than inflation. Over 20 years, you might pay $25,000 in maintenance fees on top of your original $30,000 purchase.

So you’ve spent $55,000 for 20 weeks of vacation. That’s $2,750 per week for a vacation you could have booked for $300 per night.

Want to sell? Good luck. Most timeshares sell for 10-20% of the original price if you can find a buyer at all. Many people end up paying companies thousands of dollars just to take the timeshare off their hands.

That $55,000 invested at 7% returns becomes about $170,000 over 20 years. You could take incredible vacations every year with just the investment returns and still have the principal growing.

The Insurance Scam That’s “Protecting” You Into Poverty: Whole Life Insurance

Whole life insurance is the financial equivalent of a mullet - business in the front, party in the back, and completely inappropriate for modern times.

Insurance salespeople love whole life policies because they pay huge commissions, but they’re almost always a terrible deal for you. The investment portion typically returns 2-4% per year, which barely keeps up with inflation. Meanwhile, you could invest the same money in index funds and earn 8-10% annually.

Let’s break down the math. A 30-year-old might pay $400 per month for a whole life policy. That same person could buy term life insurance for $40 per month and invest the $360 difference.

After 30 years:

- The whole life policy might have $180,000 in cash value

- The term insurance plus investing approach would have about $850,000

But it gets worse. If you need money from your whole life policy, you have to borrow against it and pay interest on your own money. If you surrender the policy early, you lose most of what you’ve paid due to surrender charges.

The insurance industry has convinced people that whole life is “forced savings” for people who can’t save on their own. But if you can’t discipline yourself to save $360 per month, you probably can’t afford the $400 whole life premium either.

Buy cheap term life insurance for protection and invest the difference in low-cost index funds. Your family gets the same protection, and you build real wealth through actual investments.

The “Safe” Investment That’s Guaranteed to Make You Poorer: Savings Accounts

Here’s something that’ll blow your mind: savings accounts are making you poorer every single year, and everyone thinks they’re being responsible.

When your money earns 0.5% interest but inflation runs 3-4%, you’re losing 2.5-3.5% of purchasing power annually. Banks love savings accounts because they get to lend your money at much higher rates while paying you almost nothing.

The “safety” of savings accounts is an illusion for long-term wealth building. Yes, you won’t lose principal, but you’re guaranteed to lose purchasing power over time. Money sitting in savings for 20 years will buy significantly less than it does today.

Let’s look at the numbers. A $50,000 savings account earning 0.5% becomes about $55,000 after 10 years. But inflation at 3% means you need $67,000 to buy what $50,000 buys today. You’ve actually lost $12,000 in purchasing power while thinking you were being safe.

That same $50,000 invested in index funds at 8% returns becomes about $108,000 after 10 years. Even accounting for inflation, you’ve more than doubled your purchasing power instead of losing it.

Emergency funds should be in savings accounts - you need 3-6 months of expenses in cash for unexpected situations. But any money beyond your emergency fund that’s sitting in savings is slowly making you poorer.

The Cryptocurrency Casino: Digital Assets That Feel Like Investments

Now let’s talk about the shiny new wealth destroyer: cryptocurrency speculation.

Don’t get me wrong - I’m not anti-crypto. But most people aren’t investing in crypto; they’re gambling. When you’re putting money into meme coins, hoping to get rich quick, or trading based on Twitter hype, you’re not building wealth. You’re playing financial roulette.

The crypto market is incredibly volatile. Bitcoin has crashed 80% multiple times. Entire coins have gone to zero overnight. People are treating it like a casino while calling it “investing.”

If you want to own some crypto as a small part of a diversified portfolio, fine. But putting your life savings into Dogecoin because someone on YouTube said it’s going to the moon? That’s not wealth building - that’s wealth destruction with extra steps.

The Real Assets That Actually Build Wealth